868 お客様のコメント

868 お客様のコメント

質問 1:

According to the FASB conceptual framework, an entity's revenue may result from:

A. A decrease in a liability from primary operations.

B. An increase in an asset from incidental transactions.

C. A decrease in an asset from primary operations.

D. An increase in a liability from incidental transactions.

正解:A

解説: (Pass4Test メンバーにのみ表示されます)

質問 2:

In single period statements, which of the following should not be reflected as an adjustment to the

opening balance of retained earnings?

A. Cumulative effect of a change from LIFO to FIFO in valuing merchandise inventory.

B. Cumulative effect of a change from the percentage of completion to the completed contract method of

accounting for long-term construction projects.

C. Effect of a failure to provide for uncollectible accounts in the previous period.

D. Effect of a decrease in the estimated useful life of depreciable equipment.

正解:D

解説: (Pass4Test メンバーにのみ表示されます)

質問 3:

In the hierarchy of generally accepted accounting principles, APB Opinions have the same authority as

AICPA:

A. Statements of Position.

B. Accounting Research Bulletins.

C. Issues Papers.

D. Industry Audit and Accounting Guides.

正解:B

解説: (Pass4Test メンバーにのみ表示されます)

質問 4:

YIV, Inc. is a multidivisional corporation, which has both intersegment sales and sales to unaffiliated

customers. YIV should report segment financial information for each division meeting which of the

following criteria?

A. Segment operating profit or loss is 10% or more of consolidated profit or loss.

B. Segment operating profit or loss is 10% or more of combined operating profit or loss of all company

segments.

C. Segment revenue is 10% or more of combined revenue of all the company segments.

D. Segment revenue is 10% or more of consolidated revenue.

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 5:

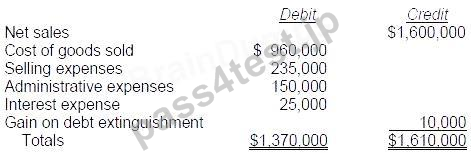

Coffey Corp.'s trial balance of Income Statement Accounts for the year ended December 31, 1988 as

follows: Coffey's income tax rate is 30%. The gain on debt extinguishment is considered a usual and

recurring part of Coffey's operations. Coffey prepares a multiple-step income statement for 1988.

Income from operations before income tax is:

A. $200,000

B. $230,000

C. $240,000

D. $190,000

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 6:

Which of the following is a generally accepted accounting principle that illustrates the practice of

conservatism during a particular reporting period?

A. Capitalization of research and development costs.

B. Accrual of a contingency deemed to be reasonably possible.

C. Reporting inventory at the lower of cost or market value.

D. Reporting investments with appreciated market values at market value.

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 7:

According to the FASB conceptual framework, which of the following is an essential characteristic of an

asset?

A. An asset is obtained at a cost.

B. The claims to an asset's benefits are legally enforceable.

C. An asset provides future benefits.

D. An asset is tangible.

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 8:

During the first quarter of 1993, Tech Co. had income before taxes of $200,000, and its effective income

tax rate was 15%. Tech's 1992 effective annual income tax rate was 30%, but Tech expects its 1993

effective annual income tax rate to be 25%. In its first quarter interim income statement, what amount of

income tax expense should Tech report?

A. $30,000

B. $50,000

C. $0

D. $60,000

正解:B

解説: (Pass4Test メンバーにのみ表示されます)

質問 9:

A material loss should be presented separately as a component of income from continuing operations

when it is:

A. A cumulative effect type change in accounting principle.

B. Not unusual in nature but infrequent in occurrence.

C. An extraordinary item.

D. Unusual in nature and infrequent in occurrence.

正解:B

解説: (Pass4Test メンバーにのみ表示されます)

According to the FASB conceptual framework, an entity's revenue may result from:

A. A decrease in a liability from primary operations.

B. An increase in an asset from incidental transactions.

C. A decrease in an asset from primary operations.

D. An increase in a liability from incidental transactions.

正解:A

解説: (Pass4Test メンバーにのみ表示されます)

質問 2:

In single period statements, which of the following should not be reflected as an adjustment to the

opening balance of retained earnings?

A. Cumulative effect of a change from LIFO to FIFO in valuing merchandise inventory.

B. Cumulative effect of a change from the percentage of completion to the completed contract method of

accounting for long-term construction projects.

C. Effect of a failure to provide for uncollectible accounts in the previous period.

D. Effect of a decrease in the estimated useful life of depreciable equipment.

正解:D

解説: (Pass4Test メンバーにのみ表示されます)

質問 3:

In the hierarchy of generally accepted accounting principles, APB Opinions have the same authority as

AICPA:

A. Statements of Position.

B. Accounting Research Bulletins.

C. Issues Papers.

D. Industry Audit and Accounting Guides.

正解:B

解説: (Pass4Test メンバーにのみ表示されます)

質問 4:

YIV, Inc. is a multidivisional corporation, which has both intersegment sales and sales to unaffiliated

customers. YIV should report segment financial information for each division meeting which of the

following criteria?

A. Segment operating profit or loss is 10% or more of consolidated profit or loss.

B. Segment operating profit or loss is 10% or more of combined operating profit or loss of all company

segments.

C. Segment revenue is 10% or more of combined revenue of all the company segments.

D. Segment revenue is 10% or more of consolidated revenue.

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 5:

Coffey Corp.'s trial balance of Income Statement Accounts for the year ended December 31, 1988 as

follows: Coffey's income tax rate is 30%. The gain on debt extinguishment is considered a usual and

recurring part of Coffey's operations. Coffey prepares a multiple-step income statement for 1988.

Income from operations before income tax is:

A. $200,000

B. $230,000

C. $240,000

D. $190,000

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 6:

Which of the following is a generally accepted accounting principle that illustrates the practice of

conservatism during a particular reporting period?

A. Capitalization of research and development costs.

B. Accrual of a contingency deemed to be reasonably possible.

C. Reporting inventory at the lower of cost or market value.

D. Reporting investments with appreciated market values at market value.

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 7:

According to the FASB conceptual framework, which of the following is an essential characteristic of an

asset?

A. An asset is obtained at a cost.

B. The claims to an asset's benefits are legally enforceable.

C. An asset provides future benefits.

D. An asset is tangible.

正解:C

解説: (Pass4Test メンバーにのみ表示されます)

質問 8:

During the first quarter of 1993, Tech Co. had income before taxes of $200,000, and its effective income

tax rate was 15%. Tech's 1992 effective annual income tax rate was 30%, but Tech expects its 1993

effective annual income tax rate to be 25%. In its first quarter interim income statement, what amount of

income tax expense should Tech report?

A. $30,000

B. $50,000

C. $0

D. $60,000

正解:B

解説: (Pass4Test メンバーにのみ表示されます)

質問 9:

A material loss should be presented separately as a component of income from continuing operations

when it is:

A. A cumulative effect type change in accounting principle.

B. Not unusual in nature but infrequent in occurrence.

C. An extraordinary item.

D. Unusual in nature and infrequent in occurrence.

正解:B

解説: (Pass4Test メンバーにのみ表示されます)

鹫尾** -

ら最新版を送られて、それげ受験してやっぱり合格だ。すごっ